Filing for bankruptcy can be a powerful tool to regain control of your finances when you’re overwhelmed by debt. But if you’re considering bankruptcy and still have a car loan, one of your first questions is likely: “Can I file bankruptcy on my car loan and still keep my car?” The short answer is yes, but it depends on your specific circumstances, the type of bankruptcy you file, and your car’s equity.

Our North Carolina bankruptcy lawyer team and South Carolina bankruptcy lawyer team can help you understand how car loans are handled during bankruptcy, the differences between Chapter 7 and Chapter 13, your legal options for keeping your vehicle, and how state-specific laws in North Carolina and South Carolina may affect your ability to protect it.

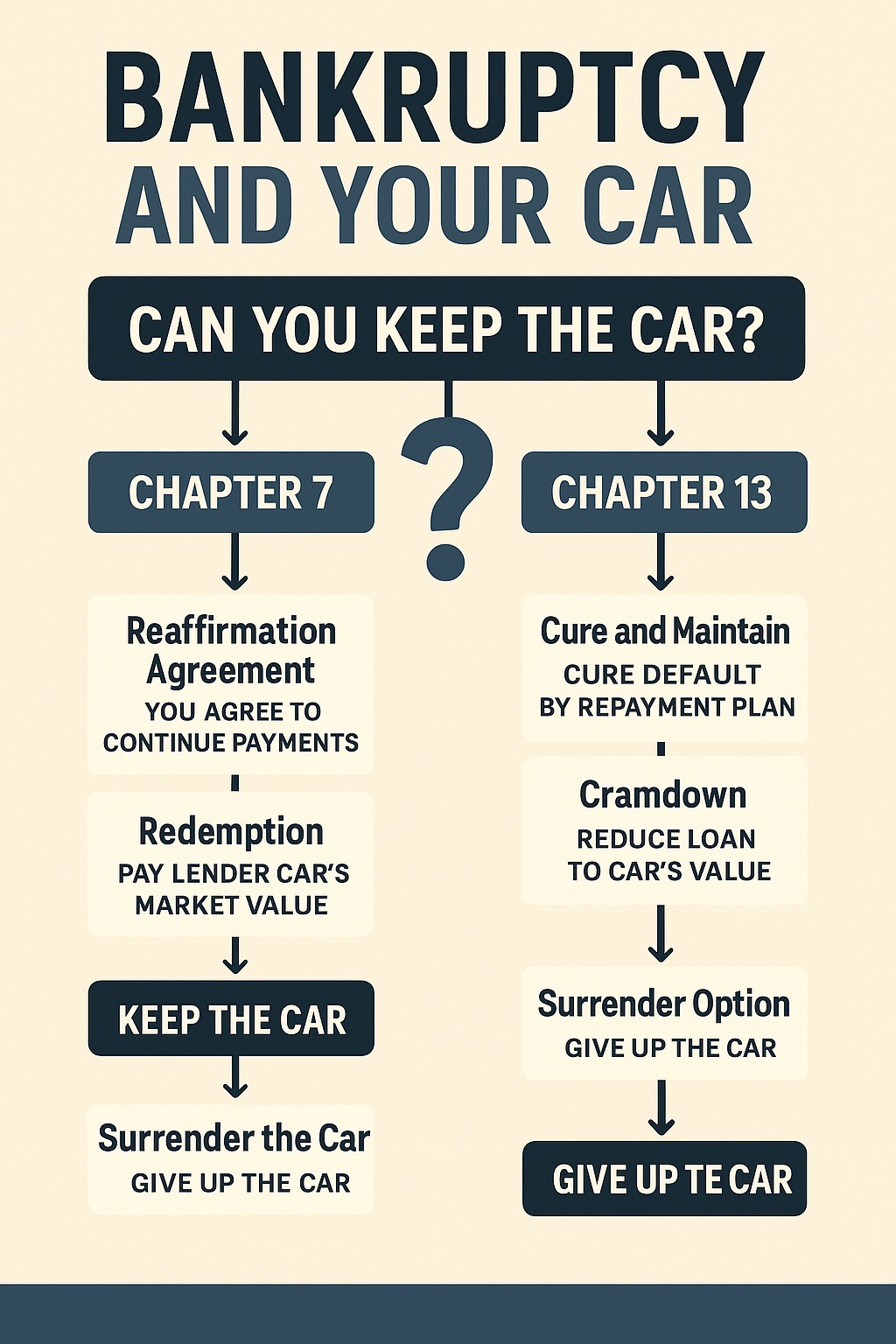

Understanding Car Loans and Bankruptcy

A car loan is a secured debt, meaning the loan is backed by collateral—in this case, the car itself. If you fall behind on your payments, the lender can repossess the vehicle. When you file for bankruptcy, the automatic stay provision prevents lenders from repossessing your car temporarily. But that doesn’t mean your obligation to pay the loan goes away. What bankruptcy can do is either discharge your personal liability on the loan (Chapter 7) or reorganize and restructure your payments (Chapter 13). Whether you get to keep the car depends on factors like the equity you have in the car, your state’s vehicle exemption laws, whether you’re current on your loan payments, and the type of bankruptcy you choose to file.

Keeping Your Car in Chapter 7 Bankruptcy

Chapter 7 is commonly referred to as “liquidation bankruptcy” and is designed to eliminate most unsecured debts quickly. It can be a lifeline for people who are struggling with credit cards, medical bills, and personal loans.

But when it comes to your car loan, Chapter 7 gives you a few key options:

1. Reaffirmation Agreement

A reaffirmation agreement means you agree to continue making payments on your car loan even after bankruptcy. In return, the lender agrees not to repossess the vehicle as long as you’re current. This option makes the most sense if you’re not behind on your payments, the car is essential for your work or family, and you can afford the monthly payments. However, if you fall behind after reaffirming, the lender can still repossess the car, and you may be held liable for any remaining balance.

2. Redemption

Under Chapter 7, you may be able to redeem your car by paying the lender a lump sum equal to the car’s current market value, not the full loan balance. This can be a great deal if you owe more than the car is worth. The challenge is that redemption requires upfront cash—something many bankruptcy filers don’t have.

3. Surrender the Car

Sometimes, the best financial decision is to walk away from the car. If the payments are too high, the car is unreliable, or you’re underwater on the loan, surrendering it in bankruptcy lets you discharge the debt and move forward.

Personal Injury Lawyer Near Me (828) 286-3866

Keeping Your Car in Chapter 13 Bankruptcy

Chapter 13, often called “reorganization bankruptcy,” is designed for people who have a steady income but need time and structure to catch up on debts. Under this plan, you create a 3- to 5-year repayment plan to address debts, including car loans.

Chapter 13 offers some powerful advantages for keeping your car, especially if you’re behind on payments or upside down on your loan.

1. Cure and Maintain

If you’re behind on your car loan, Chapter 13 allows you to “cure” the default by spreading out your missed payments over the life of the repayment plan. As long as you stay current on both your monthly payments and the repayment plan, you can keep your car.

2. Cramdown

One of the most powerful tools in Chapter 13 is the cramdown, which allows you to reduce the loan balance to the current market value of the car—if you’ve owned the vehicle for more than 910 days. The remaining balance is treated as unsecured debt and may be discharged after completing the repayment plan. This is especially useful if you’re upside down on your loan and the car has depreciated significantly.

3. Surrender Option

Just like in Chapter 7, you still have the option to surrender the car in Chapter 13 if it no longer makes financial sense to keep it.

State Vehicle Exemption Laws: North Carolina and South Carolina

Every state allows bankruptcy filers to protect a certain amount of equity in their vehicle through exemption laws. If your equity in the car is within your state’s exemption limit, you can usually keep the vehicle.

North Carolina Vehicle Exemption:

North Carolina allows individuals filing bankruptcy to exempt up to $3,500 in equity in one motor vehicle. If the vehicle is jointly owned by a married couple filing jointly, they may be able to double this amount. Additionally, North Carolina offers a wildcard exemption of up to $5,000 (depending on unused portions of other exemptions), which can be applied to protect more vehicle equity if needed.

South Carolina Vehicle Exemption:

South Carolina residents can exempt up to $6,325 in vehicle equity (as of 2023, adjusted every few years). Like North Carolina, a wildcard exemption of $5,000 may be available if the homestead exemption is not fully used. These exemptions are especially helpful in Chapter 7 cases where the trustee would otherwise sell a car with excess equity to pay creditors.

Keep in mind that these exemption limits apply to equity, not the car’s full value. So if your car is worth $15,000 and you still owe $12,000, your equity is only $3,000—and likely protected under either state’s laws.

What Happens If You’re Leasing a Car?

If your car is leased rather than purchased with a loan, you still have options in bankruptcy. You can assume the lease, keep making payments, and continue using the car, or you can reject the lease, return the car, and discharge any penalties or remaining payments. Leasing is different from ownership—you don’t have equity, so exemption laws don’t apply, but bankruptcy gives you flexibility either way.

Key Factors That Influence Whether You Can Keep Your Car

Here’s a quick checklist of what determines whether you’ll keep your car in bankruptcy:

-

Are you current on payments? If yes, reaffirmation (Chapter 7) or regular payments (Chapter 13) may allow you to keep it.

-

Is there equity in the car, and is it covered by your state’s exemption limits?

-

Is the car essential for work or daily life?

-

Can you realistically afford ongoing payments?

-

Are you upside down on the loan? Cramdowns in Chapter 13 or redemptions in Chapter 7 may help.

Final Thoughts: Yes, You Can Keep Your Car—But Plan Carefully

Filing for bankruptcy doesn’t automatically mean giving up your car. In both Chapter 7 and Chapter 13, there are strategies that can help you keep your vehicle—whether it’s through reaffirming the loan, redeeming the car, catching up on payments, or using a cramdown to restructure the balance.

However, keeping your car in bankruptcy is not always the best financial choice. If the loan terms are unfavorable, the car isn’t reliable, or the payments are unsustainable, surrendering the car and discharging the debt may put you in a stronger long-term position.

If you’re considering bankruptcy in North Carolina or South Carolina and are concerned about your car, it’s essential to contact a local bankruptcy attorney like Farmer Morris. Our lawyers can explain how your state’s exemption laws apply to your situation, help you choose the right bankruptcy chapter, and guide you through the process of protecting your vehicle while eliminating debt.